Choosing the right publishing house is a crucial step in an author’s journey. The right publisher can help elevate your book, while the wrong fit can lead to frustration. To make the best choice, start by researching publishers that specialize in your genre. A publisher familiar with your type of work will know how to market it effectively and reach your target audience.

Next, consider the difference between traditional and independent publishing. Traditional publishers often provide broader distribution and more support, but they can be selective. Independent presses may offer more creative freedom and a closer working relationship, while self-publishing gives you complete control over the process.

Also, pay attention to the level of editorial and marketing support a publisher offers. A strong editorial team is key to refining your manuscript, and a good marketing plan will ensure your book reaches the right readers. Review contract terms carefully—royalties, advances, and rights to future work can have a long-term impact on your career.

Finally, consider a publisher’s reputation and whether you feel comfortable working with them. The relationship between author and publisher should be collaborative and aligned with your vision for the book. Ultimately, finding the right publishing house is about more than just getting your book into print; it’s about finding a partner to help bring your story to the world.

Becoming a published author is a powerful way to boost your professional standing and open new opportunities. Publishing a book, whether fiction or non-fiction, positions you as an expert in your field, enhancing your credibility and authority. This newfound recognition can lead to invitations for speaking engagements, consulting roles, and media appearances, all of which expand your network and career possibilities.

A book also strengthens your personal brand. It allows you to showcase your expertise and differentiate yourself in a crowded industry. Many professionals use their published work as a platform for building long-term influence and thought leadership.

Beyond personal branding, writing a book sharpens your communication skills. The discipline and creativity required to craft a compelling narrative can improve how you express ideas in other professional settings, from presentations to reports.

While publishing offers new revenue streams—through book sales, workshops, or speaking engagements—it also provides intangible benefits like confidence and a sense of accomplishment. The impact of being a published author often extends far beyond the initial launch, leaving a lasting professional legacy.

Tenet Consultores highlights the importance of the country’s first historical publication on ITFs, including IFPEs and IFCs

Paula Marmolejo – Economics Analyst Victor Silva – Financial Analyst

The Comisión Nacional Bancaria y de Valores’ (CNBV) first publication on Financial Technology Institutions (ITFs by its acronym in Spanish) marks a significant milestone for the fintech sector in Mexico. This report provides a comprehensive view of the performance of Instituciones de Fondos de Pago Electrónico (IFPE) and Instituciones de Financiamiento Colectivo (IFC), which not only improves transparency but also allows for measuring the growth and maturity of these institutions within the Mexican financial ecosystem.

The CNBV’s publication of this data not only reflects the evolution and maturity of the fintech sector but also underscores the need to continue promoting these institutions so that they continue to offer accessible, innovative, and secure financial services, contributing significantly to the country’s economic development. The complete information can be found at the following link: Instituciones de Tecnología Financiera – CNBV.

ITF’s DESCRIPTION

IFPEs allow payments, purchases, and money transfers to be made digitally. These institutions can operate in local currency, foreign currency, and virtual assets.

IFCs enable fundraising from multiple investors or lenders to finance projects, businesses, or initiatives. These institutions can operate using different financing models, such as collective loans, collective capital, donations, and rewards.

FIRST PUBLICATION OF HISTORICAL DATA

On October 7, 2024, the CNBV made its first historical publication on Mexican ITFs, which includes data on IFPEs and IFCs from January 2021 to December 2023.

The ITFs published by the authority are divided as follows according to their status and compliance in the delivery of information at the end of 2023.

IFPE: There were 50 authorized entities, of which 37 were in operation. Of the 37 IFPEs in operation, 89% submitted information in due time and form. Within this sector, the number of IFPEs in operation has grown by 68% annually.

IFC: There were 21 authorized entities, of which 17 were in operation. Of the latter, 94% submitted information in due time and form.

KEY PLAYERS AMONG ITFs

IFPE: STP (Sistema de Transferencias y Pagos) leads in fundraising with 35.42%. Second place goes to Mercado Pago with 30.10% of the total. In third place is OXXO’s SPIN with 12.16%. Together, these three entities hold 77.68% of the electronic payment funds issued.

IFC: Play Business leads in institutions’ assets with 22.26%. Cien Ladrillos is in second place with 13.39%, followed by Yo Te Presto with 12.50%. Together, these three institutions hold 48.15% of the institutions’ assets.

Tenet Consultores resalta la importancia de la primera publicación histórica sobre las ITF en el país, que incluye a las IFPE y a las IFC

Paula Marmolejo – Analista en economía Victor Silva – Analista financiero

La primera publicación de la Comisión Nacional Bancaria y de Valores (CNBV) sobre las Instituciones de Tecnología Financiera (ITF) marca un hito significativo para el sector fintech en México. Este informe proporciona una visión integral sobre el desempeño de las Instituciones de Fondos de Pago Electrónico (IFPE) y las Instituciones de Financiamiento Colectivo (IFC), lo que no solo mejora la transparencia, sino que también permite medir el crecimiento y la madurez de estas instituciones dentro del ecosistema financiero mexicano.

La publicación de estos datos por parte de la CNBV no solo refleja la evolución y madurez del sector fintech, sino que también subraya la necesidad de seguir impulsando a estas instituciones para que continúen ofreciendo servicios financieros accesibles, innovadores y seguros, contribuyendo de manera significativa al desarrollo económico del país. La información completa puede encontrarse en el siguiente enlace: Instituciones de Tecnología Financiera – CNBV.

DESCRIPCIÓN DE LAS ITF

Las IFPE permiten realizar pagos, compras y envíos de dinero de manera digital. Estas instituciones pueden operar en moneda nacional, moneda extranjera y activos virtuales.

Las IFC permiten la recaudación de fondos de múltiples inversores o prestamistas para financiar proyectos, empresas o iniciativas. Estas instituciones pueden operar en distintos modelos de financiamiento, como préstamos colectivos, capital colectivo, donaciones y recompensas.

PRIMERA PUBLICACIÓN DE DATOS HISTÓRICOS

El 7 de octubre de 2024, la Comisión Nacional Bancaria y de Valores (CNBV) realizó su primera publicación histórica sobre las ITF en México, la cual incluye datos sobre IFPE e IFC de enero de 2021 a diciembre de 2023.

Las ITF publicadas por la autoridad se dividen de la siguiente manera conforme a su estatus y a su cumplimiento en la entrega de la información al cierre de 2023.

IFPE: Se contaba con 50 entidades autorizadas, de ellas 37 se encontraban en operación. De las 37 IFPE que se encuentran operando, 89% presentaron información en tiempo y forma. Dentro de este sector, ha habido un crecimiento de 68% anual con respecto al número de IFPE en operación.

IFC: Se contaba con 21 entidades autorizadas de ellas 17 se encontraban en operación. De estas últimas, el 94% presentaron información en tiempo y forma.

JUGADORES CLAVE ENTRE LAS ITF

IFPE: STP (Sistema de Transferencias y Pagos) lidera la captación con un 35.42%. El segundo lugar lo ocupa Mercado Pago con un 30.10% del total. En tercer lugar se encuentra SPIN de OXXO con 12.16%. En conjunto estas tres entidades mantienen el 77.68% de los fondos de pago electrónicos emitidos.

IFC: Play Business lidera el monto de activos de las instituciones con un 22.26%. En segundo lugar se encuentra Cien Ladrillos con 13.39%, seguido de Yo Te Presto con 12.50%. En conjunto estas tres entidades mantienen el 48.15% de activos de las entidades.

Tenet Consultores informa acerca de la resolución que modifica las disposiciones de carácter general aplicables a estas instituciones

Xóchitl Juárez Jiménez – Líder de consultoría contable

La Comisión Nacional Bancaria y de Valores (CNBV) anunció la modificación a las Disposiciones de Carácter General Aplicables a las Instituciones de Tecnología Financiera, en las que se agrega, en el artículo 100, el Reporte Regulatorio con la serie R-24 “Información operativa” con el reporte G-2470 Información relativa a Clientes y Operaciones. Dicho reporte deberá ser entregado dentro de los 10 días hábiles del mes inmediato siguiente al periodo que se reporta mediante su transmisión vía electrónica utilizando el SITI.

La modificación, publicada en el Diario Oficial de la Federación del 2 de septiembre, busca la explotación eficiente de la información operativa de las instituciones de fondos de pago electrónico para la generación automatizada de indicadores o métricas de análisis, así como de informes de supervisión estandarizados y la incorporación de validadores regulatorios automatizados; adaptados a las necesidades específicas y con la flexibilidad requerida para llevar a cabo la supervisión tecnológica de las Instituciones de Tecnología Financiera.

Tiene como finalidad garantizar que estas instituciones puedan operar de manera eficiente y segura, promoviendo al mismo tiempo la protección de los usuarios, creando con esto la confianza en el sector Fintech.

MODIFICACIÓN

Se agrega, en el artículo 100, el Reporte Regulatorio con la serie R-24 “Información operativa” con el reporte G-2470 Información relativa a Clientes y Operaciones, como a continuación se detalla:

Información de Clientes

Información de cuentas de Clientes

Información de cuentas para el manejo de recursos de Clientes

Información de cuentas para el manejo de recursos propios

Saldos y movimientos de cuentas de Clientes

Saldos y movimientos de cuentas para el manejo de recursos de Clientes

Sobregiros

Comisiones

Dicho reporte deberá ser entregado dentro de los 10 días hábiles del mes inmediato siguiente al periodo que se reporta, de conformidad en los establecido en el artículo 101, inciso a.

La información se deberá enviar a la Comisión Nacional Bancaria y de Valores, mediante su transmisión vía electrónica utilizando el SITI. En caso de que no exista información de algún reporte, las instituciones deberán realizar el envío vacío, funcionalidad que está disponible en dicho sistema. En el caso del reporte regulatorio correspondiente a la Serie R24 G-2470 del Anexo 19, se deberá apegar al formato y especificaciones de reporte y transferencia de información que la propia CNBV indique a las instituciones de fondos de pago electrónico, lo anterior con apego a lo establecido en el primer párrafo del artículo 103, de las Disposiciones.

ENTRADA EN VIGOR

Esta modificación entrará en vigor al día siguiente de su publicación en el Diario Oficial de la Federación, teniendo como plazo hasta el 1 de enero de 2025 para realizar las acciones necesarias a efecto de presentar el reporte regulatorio.

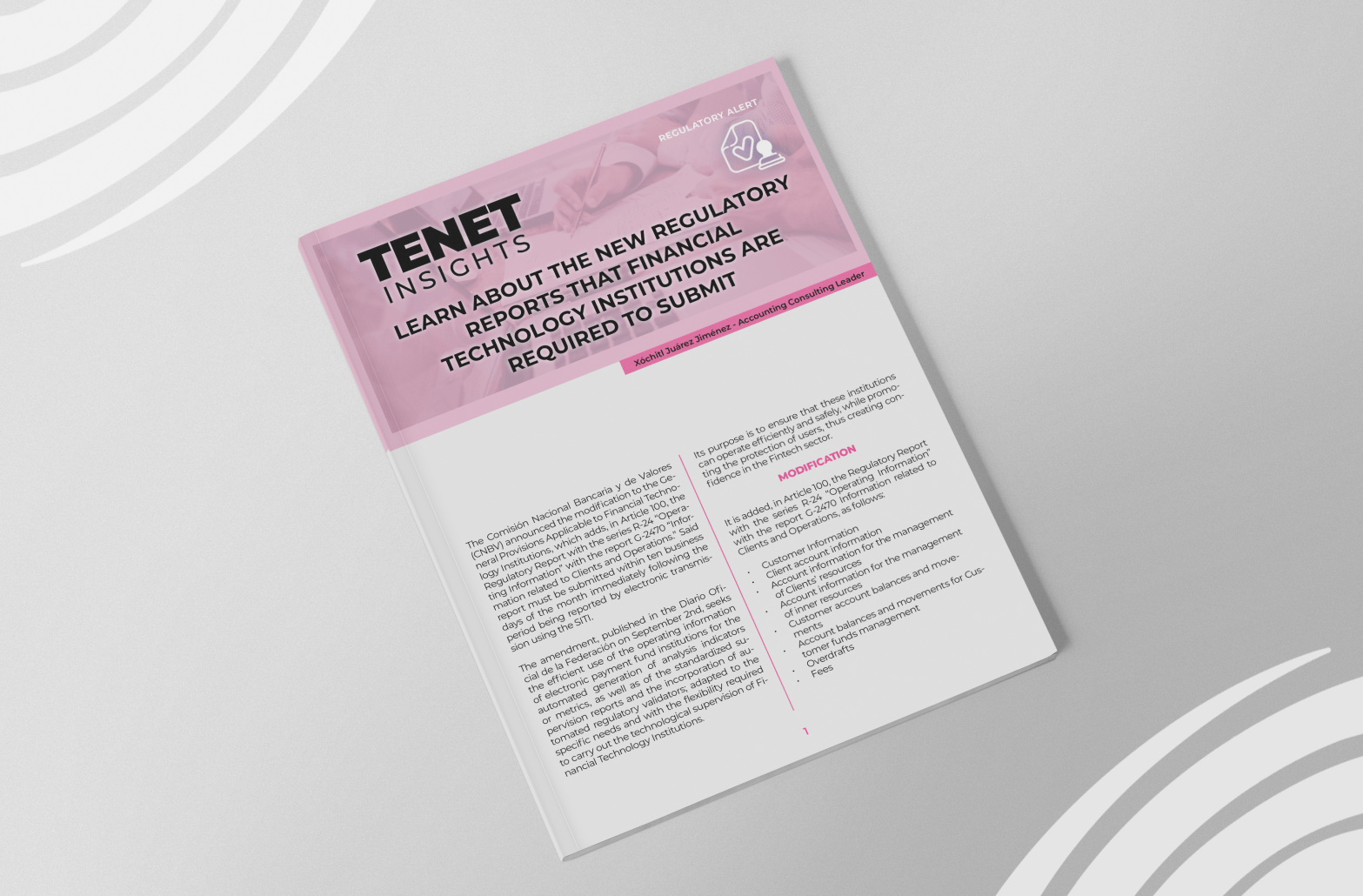

Tenet Consultores informs about the resolution that modifies the general provisions applicable to these institutions

he Comisión Nacional Bancaria y de Valores (CNBV) announced the modification to the General Provisions Applicable to Financial Technology Institutions, which adds, in Article 100, the Regulatory Report with the series R-24 “Operating Information” with the report G-2470 “Information related to Clients and Operations.” Said report must be submitted within ten business days of the month immediately following the period being reported by electronic transmission using the SITI.

The amendment, published in the Diario Oficial de la Federación on September 2nd, seeks the efficient use of the operating information of electronic payment fund institutions for the automated generation of analysis indicators or metrics, as well as of the standardized supervision reports and the incorporation of automated regulatory validators; adapted to the specific needs and with the flexibility required to carry out the technological supervision of Financial Technology Institutions.

Its purpose is to ensure that these institutions can operate efficiently and safely, while promoting the protection of users, thus creating confidence in the Fintech sector.

MODIFICATION

It is added, in Article 100, the Regulatory Report with the series R-24 “Operating Information” with the report G-2470 Information related to Clients and Operations, as follows:

Customer Information

Client account information

Account information for the management of Clients’ resources

Account information for the management of inner resources

Customer account balances and movements

Account balances and movements for Customer funds management

Overdrafts

Fees

This report must be submitted within 10 business days of the month immediately following the period being reported, in accordance with the provisions of Article 101, paragraph a.

The information must be sent to the Comisión Nacional Bancaria y de Valores (CNBV) by electronic transmission using the SITI. In the event that there is no information of any report, the institutions must send the information empty, functionality that is available in said system. In the case of the regulatory report corresponding to Series R24 G-2470 of Annex 19, it must adhere to the format and specifications for reporting and transfer of information that the CNBV itself indicates to the electronic payment fund institutions, in accordance with the provisions of the first paragraph of article 103 of the Provisions.

EFFECTIVE DATE

This modification will become effective the day after its publication in the Diario Oficial de la Federación, with a deadline of January 1st, 2025 to carry out the necessary actions in order to submit the regulatory report.

«Conoce los nuevos reportes regulatorios que deben presentar las Instituciones de tecnología financiera»

Tenet Consultores informa acerca de la resolución que modifica las disposiciones de carácter general aplicables a las instituciones de tecnología financiera.

Tenet Consultores informs about the changes to the General Provisions referred to in Article 115 of the Law of Credit Institutions (Ley de Instituciones de Crédito)

The Mexican Secretaría de Hacienda y Crédito Público (SHCP), with the prior opinion of the Comisión Nacional Bancaria y de Valores (CNBV), announced changes to the Ley de Instituciones de Crédito, which modify the regulation on money laundering prevention.

The resolution that amends, adds, and repeals several of the general provisions referred to in Article 115 of the Ley de Instituciones de Crédito was published in the Diario Oficial de la Federación on August 28th, 2024.

Among the main changes that will affect credit institutions in Mexico are modifications in the identification of clients and the opening of accounts, as well as changes in the requirements for transaction reports, and the annual submission of information from the operating questionnaire, all with a focus on improving the prevention of transactions with resources of illicit origin and the financing of terrorism.

The new provisions update the definitions of Client, Device, and Risk, among others, and introduce the definition of the Interim Compliance Officer.

On the other hand, more IDs have been accepted to identify clients, such as the voting credentials issued by consular offices. And the identification requirements for federal, state, and municipal public agencies and entities classified with a Risk Level other than low, as well as for suppliers, have been also modified.

On the other hand, the requirement to prove the legal existence of federal, state, and municipal public agencies and entities, as well as other legal entities, has been eliminated.

However, there will be more requirements to identify public agencies and entities classified with a Risk Level other than low, as well as to identify foreign nationals outside the country.

There are also increased requirements to identify co-owners and authorized third parties in accounts opened by clients, as well as beneficiaries. In the case of trusts, it establishes how to identify the members of the technical committee or equivalent governing body, when the credit institutions do not act as trustees.

The requirements for non-face-to-face identification have been modified, eliminating the possibility of doing so for foreign customers and other specific groups such as authorized third-party course providers and beneficiaries.

There is also an obligation to conduct a face-to-face interview or apply any of the authorized technological identification mechanisms when the transactional level of low-risk accounts is exceeded, and this level must be defined at the beginning of the relationship and through the automated system.

Credit Institutions will face increased requirements when opening accounts or entering into agreements with Clients that, due to their characteristics, could generate a high Risk Level.

And now, international fund transfers must be reported to the SHCP in the event that a credit institution is the holder of a Omnibus Account opened in another credit institution or in any Obligated Entity.

The requirements for the transactions ID with Sociedades Financieras de Objeto Múltiple no reguladas (Sofomes), Exchange Centers and Money Transmitters have also been modified.

Institutions would also be required to establish a Compliance Manual with specific criteria, measures, and procedures against terrorist financing as a crime.

In summary, these changes will mainly affect customer identification and verification, risk management, compliance, and transaction reporting procedures.

The objective is to strengthen prevention and control practices in financial institutions, ensuring a robust framework for the identification and management of risks associated with money laundering and terrorist financing.

These changes will require technological and operational adjustments by the institutions to comply with the new standards, as well as more sophisticated monitoring of operations, reporting and auditing requirements.

Institutions will need to adapt their policies, procedures, and systems to meet the new requirements and ensure compliance with the updated regulations.

Alejandra Onofre – Líder de Consultoria en prevención de lavado de dinero

La Secretaría de Hacienda y Crédito Público (SHCP), contando con la previa opinión de la Comisión Nacional Bancaria y de Valores (CNBV), anunció cambios a la Ley de Instituciones de Crédito, que modifican la regulación de prevención de lavado de dinero (PLD).

La resolución que reforma, adiciona y deroga diversas de las Disposiciones de carácter general a que se refiere el artículo 115 de la Ley de Instituciones de Crédito fue publicada en el Diario Oficial de la Federación el 28 de agosto de 2024.

Entre los principales cambios que afectarán a las Instituciones de Crédito en México destacan modificaciones en la identificación de clientes y en la apertura de cuentas, así como cambios en los requisitos para los reportes de operaciones y remitir anualmente la información del cuestionario de operatividad, todo esto con un enfoque en mejorar la prevención de operaciones con recursos de procedencia ilícita y financiamiento al terrorismo.

Las nuevas disposiciones actualizan las definiciones de Cliente, Dispositivo y Riesgo, entre otras, e introducen la definición del Oficial de Cumplimiento Interino.

Por otro lado, se amplían las formas aceptadas para identificar clientes, como la credencial para votar expedida por las oficinas consulares. Y también se modifican los requisitos de identificación para dependencias y entidades públicas federales, estatales y municipales clasificadas con un grado de riesgo distinto al bajo, así como para los proveedores de recursos.

Por otra parte, se elimina el requisito para acreditar la legal existencia de dependencias y entidades públicas federales, estatales y municipales, así como de otras personas morales.

Sin embargo, existirán más requisitos para identificar a las dependencias y entidades públicas clasificadas con un Grado de Riesgo distinto al bajo, así como para identificar a propietarios de nacionalidad extranjera que se encuentren fuera del país.

También se exigen mayores requisitos para identificar a los cotitulares y terceros autorizados en cuentas abiertas por clientes, así como a los beneficiarios. En el caso de los fideicomisos, se establece la forma de identificar a los miembros del comité técnico u órgano de gobierno equivalente, cuando las instituciones de crédito no actúen como fiduciarias.

Se modifican los requisitos para la identificación no presencial, eliminando la posibilidad de realizarla para clientes extranjeros y otros grupos específicos como proveedores de recursos terceros autorizados y beneficiarios.

También se contempla la obligación de realizar entrevista presencial o aplicar alguno de los mecanismos tecnológicos de identificación cuando se sobrepase el nivel transaccional de las cuentas de bajo riesgo, y este grado deberá definirse al inicio de la relación y a través del sistema automatizado.

Las Instituciones de Crédito enfrentarán mayores requisitos al abrir cuentas o celebrar contratos con Clientes que, por sus características, pudieran generar un Grado de Riesgo alto.

Y ahora se deberán reportar a la SHCP las transferencias internacionales de fondos en el caso en que una institución de crédito sea titular de una Cuenta Concentradora abierta en otra institución de crédito o en algún Sujeto Obligado.

También se modifican los requisitos para la identificación de operaciones con Sociedades Financieras de Objeto Múltiple no reguladas, Centros Cambiarios y Transmisores de Dinero. Las instituciones también estarían obligadas a establecer un Manual de Cumplimiento criterios, medidas y procedimientos específicos para el delito de financiamiento al terrorismo.

En resumen, estos cambios afectan principalmente la identificación y verificación de los clientes, la gestión de riesgos, los procedimientos de cumplimiento y de reportes de operaciones. El objetivo es fortalecer las prácticas de prevención y control en las instituciones financieras, garantizando un marco robusto para la identificación y manejo de riesgos asociados con el lavado de dinero y el financiamiento al terrorismo.

Estos cambios exigirán ajustes tecnológicos y operativos por parte de las instituciones para cumplir con los nuevos estándares, así como un monitoreo más sofisticado en las operaciones, los requisitos de reportes y auditorías. Las instituciones deberán adaptar sus políticas, procedimientos y sistemas para cumplir con los nuevos requisitos y asegurar la conformidad con las normativas actualizadas.%. En segundo lugar se encuentra Cien Ladrillos con 13.39%, seguido de Yo Te Presto con 12.50%. En conjunto estas tres entidades mantienen el 48.15% de activos de las entidades.